Parul University B-TECH Admissions 2026

ADMISSIONS CLOSING ON 15th JULY | APPLY NOW | India's youngest NAAC A++ accredited University | NIRF rank band 151-200 | 2200 Recruiters | 45.98 Lakhs Highest Package

Studying Abroad vs Studying in Foreign Universities in India- Which is better for you in 2026? If you want to get a deeper understanding of which study option is worth it for you between these two, then you have arrived at the right place. This article will provide a detailed evaluation of the actual cost and risk involved in Studying Overseas and studying Foreign Universities in India, primarily from the Indian students & parents' perspective.

Watch The Video Here

When you decide to study in a foreign country, the cost is guaranteed. Besides paying tuition fees, there are other fixed expenses like living expenses, insurance, and travel expenses; these are often very high or may be more than the tuition fees. So the cost of studying abroad is guaranteed, but the outcome is uncertain because it depends on various factors like:

Reputation of the university and relevance of the course

Job market scenario in that country

Visa & work permit policies

Your networking & adaptability

For example, even spending so much on study in countries like the UK, Canada, and US, there are various challenges faced by the students, such as economic downturns or job sponsorships. So, even if you pay up front, the ROI remains uncertain.

But if you are financially capable, open to uncertainty, and want to experience global exposure, then studying abroad can pay off. But if you want to get a globally recognized degree, considering the financial safety, then studying in foreign universities in India is a better option for you.

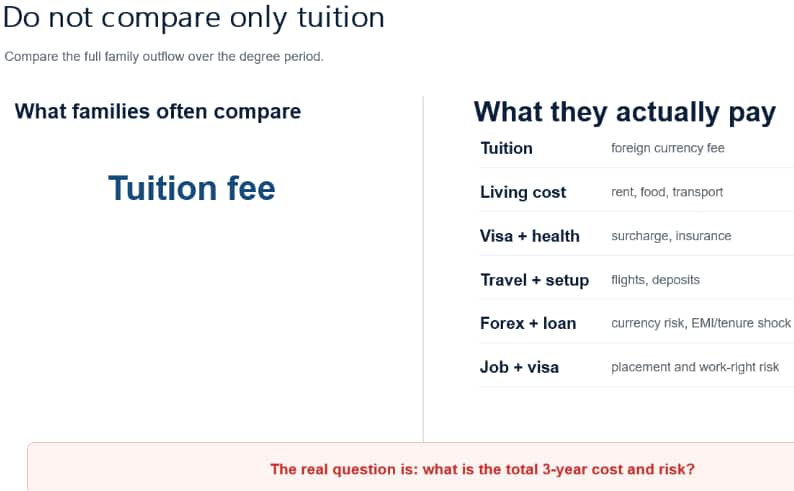

Families often compare the tuition fee, but the total cost is not determined only by the tuition fee; actual costs and risks involved in a three-year course from abroad are beyond the tuition fee.

Key comparison is highlighted between studying overseas and studying in foreign campuses setting up in India, which offer the same value degree at relatively lower risk and cost, and are UGC approved.

Living cost (food, transport, housing)

Fluctuations in forex and loan repayment risks

Medical & health insurance cost

Set up and travel expenses (relocation and periodic home visits)

Visa fees

ADMISSIONS CLOSING ON 15th JULY | APPLY NOW | India's youngest NAAC A++ accredited University | NIRF rank band 151-200 | 2200 Recruiters | 45.98 Lakhs Highest Package

NAAC A+ Grade | Ranked 503 Globally (QS World University Rankings 2026)

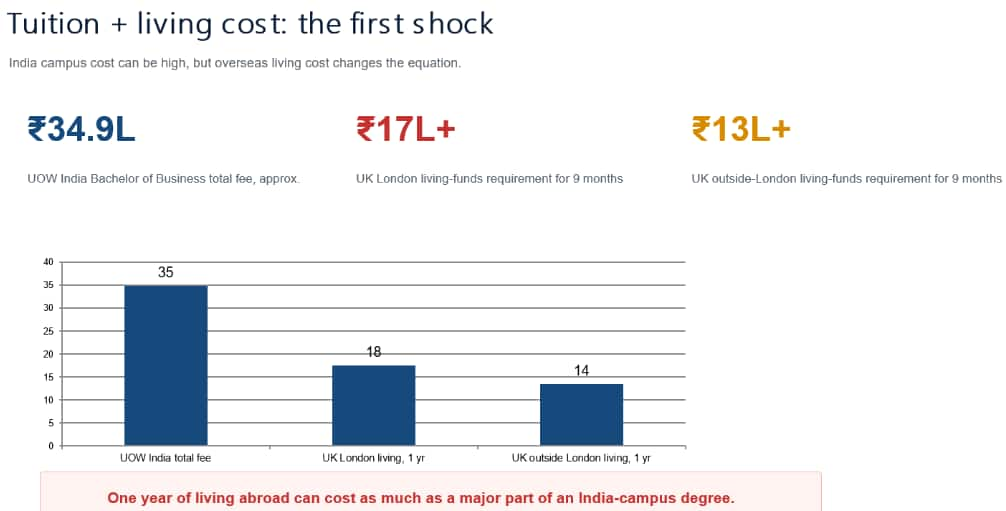

The total fees for foreign campuses in India, like the UOW India Bachelor of Business, are approximately Rs. 34.9 Lakhs. Foreign campuses established in India also offer scholarships of around 25 to 100 per cent.

The annual cost of living in the UK London is more than Rs. 17 Lakhs, and the three-year cost of living will be around Rs. 50 to 60 Lakhs excluding tuition fees.

The annual cost of living in the UK outside London is more than Rs. 13 Lakhs, and the total cost of living will be around Rs. 40 to 50 Lakhs.

Hence, the cost of living abroad alone is equivalent to or more than the total fee of a foreign campus in India. Although the foreign universities in India are UGC approved, the degree value is the same in both cases: studying in foreign campuses in India and studying abroad, but the global immersion is not the same.

These are access costs - they do not improve the degree | ||

Category | Foreign University in India Requirement | Abroad Requirement |

UK visa | Not required for full India study | Student visa from India: about ₹74,006 |

UK health | Usually domestic health cover | IHS: £776 per year for students |

Australia | No Australia student visa | Student visa: AUD 2,000 from July 2025 |

Canada | No Canada study permit | Proof of living funds: CAD 22,895 from Sept 2025 |

Before the student attends first class abroad, the family may already face visa fees, health surcharges, insurance, blocked funds, and relocation costs.

The fees for a UK visa is approximately Rs. 74,006.

The UK health surcharge is around Rs. 3.0 Lakhs for three years.

The fees for the Australian visa are approximately in the range of Rs. 1.5 to 2 Lakhs.

The living costs in Canada require financial proof of funds of around Canadian Dollar 22,895 (approximately over Rs. 15 Lakhs).

Ranked #29 in Engineering Category in India by NIRF Ranking 2025 | Highest CTC 1.23 Cr | Average 11.38 LPA | Scholarships Available

40 LPA Highest Package | Up to 100% Scholarship worth 24 Crore via GUTS exam

The cost of health and visa is additional and is often overlooked.

Currency | Apr/My 2024 | Apr/May 2026 | Increase |

USD | ₹83.50 | ₹95.24 | +14.1% |

GBP | ₹104.30 | ₹128.20 | +22.9% |

AUD | ₹54.80 | ₹68.37 | +24.8% |

CAD | ₹61.02 | ₹69.81 | +14.4% |

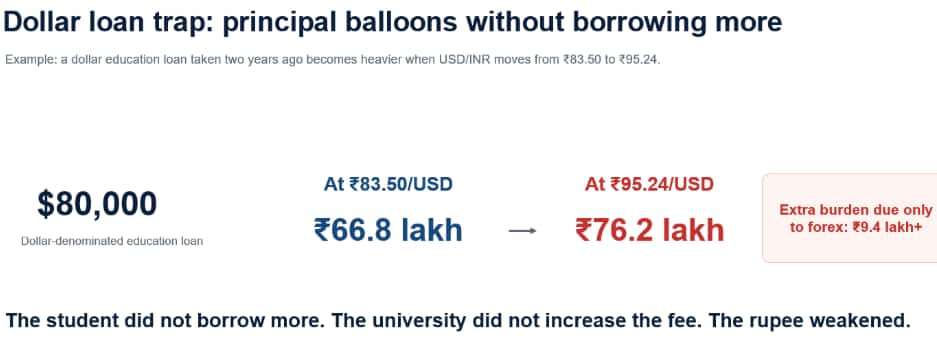

The tuition fee and the cost of living are charged in foreign currencies and paid after converting it into the local currency. So, even if the university fee is unchanged, the rupee cost can rise sharply. As there is a significant increase of 14.1 per cent in actual rupee against USD, ranging from 2024 to 2026. Similarly, loans taken at GBP, AUD, and CAD range in 2024 now cost more due to the rupee weakening. This is why a foreign fee is not a fixed rupee commitment. The burden of overall payment eventually increases, and this risk is often overlooked by many families, leading to financial pressure.

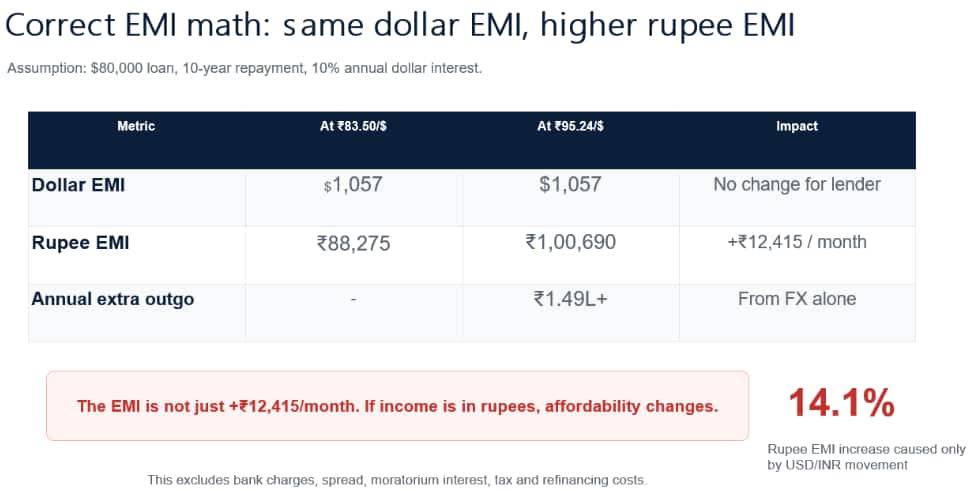

For example, An $80,000 dollar education loan taken at ₹83.5/USD two years ago now costs more when USD/INR moves from Rs. 83.50 to Rs. 95.24 due to the rupee weakening. The student did not borrow more. The university did not increase the fee. The rupee weakened.

Rupee EMI has increased by approximately Rs. 12,415 per month. So, this results in extended loan repayment tenures and higher EMIs.

Scenario | Rupee outgo | Dollar repayment | Approx. tenure |

Original plan | ₹88,275/month | $1,057/month | 120 months |

After USD rises to ₹95.24 | ₹88,275/month | $927/month | 153 months |

Extra time | - | - | +33 months |

Repayment tenure extended from 120 months to 153 months. The tenure stretches to an additional 33 months. Keeping the original rupee EMI means the dollar payment falls, and tenure stretches. The same rupee EMI does not solve the problem. It converts EMI shock into tenure shock and extra interest.

Scenario | Tenure | Monthly rupee EMI | Total rupee outgo |

Original plan | 120 months | ₹88,275 | ₹1.06 crore |

Keep the same rupee EMI after FX shock | 153 months | ₹88,275 | ₹1.35 crore |

Additional burden | +33 months | - | +₹29 lakh |

FX stress converts a 10-year plan into a longer and costlier repayment path. Forex risk not only increases the monthly EMI. It can extend repayment and inflate the total interest.

Foreign universities in India offer scholarships to attract the top talented candidates.

Merit-based scholarships result in a substantial fee reduction.

Don’t just compare the brochure fees; compare net fees after scholarships.

The fees for the foreign campuses in India are comparable with the fees charged by some of the private liberal arts universities.

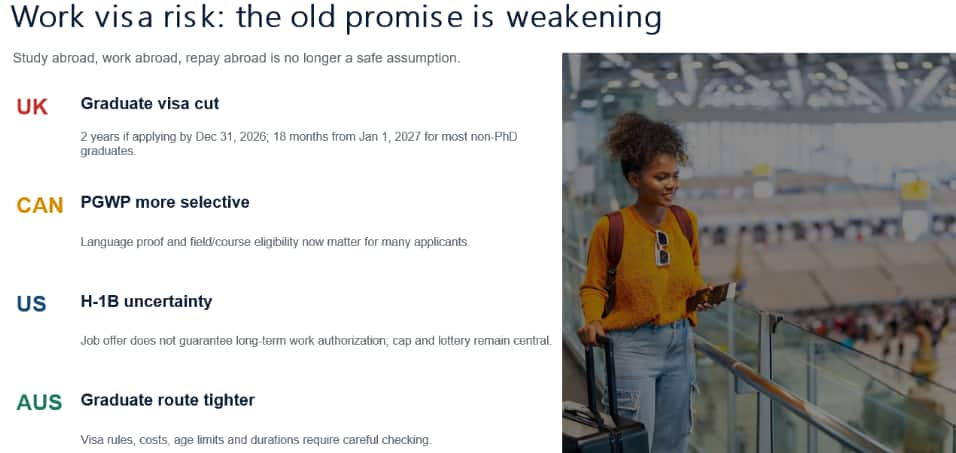

Post study work visa periods are becoming shorter. In the UK, the graduate visa became shorter from two-years to 18 months.

Strict visa rules and intense competition make it harder to secure jobs abroad.

Domestic applicants are given priority by the employers because of the visa-related complexities.

Countries like the US have uncertain H-1B visa processes. Job offer doesn’t assure long-term work permit, involving cap and lottery selection.

Post study work visa rules in Australia and Canada have become stricter.

The expectations that students will work abroad and repay loans in foreign currency is progressively becoming uncertain.

Many graduates may end up returning to India and earning in rupees but have to repay loans in foreign currency, leading to more financial risk.

Placement Risk: Tuition fee is guaranteed, rent is guaranteed, loan is guaranteed, but the job is not guaranteed.

1- No guaranteed centralized placement

2- Internships and referrals matter

3- Local students may have a visa advantage

4- Employers may avoid visa compliance

5- Visa clock creates pressure

Category | India campus | Going abroad |

Living cost | Lower: Indian rent/hostel/food | High: foreign rent, deposits, daily costs |

Visa/health | Usually avoided | Visa fee + health surcharge + insurance |

Forex | Lower exposure, but check billing currency | Fee/living/loan in foreign currency |

Dollar loan | Often avoidable | Principal, EMI and tenure can balloon |

Work visa | Not central to degree cost | Outcome depends on country rules |

Job risk | Still exists, without foreign debt | Job and sponsorship not guaranteed |

This table provides a comparison between Foreign campuses in India and going abroad for study. Check out this table for the comparison related to living cost, visa or health, forex, dollar loan, work visa and job risk involved in both cases.

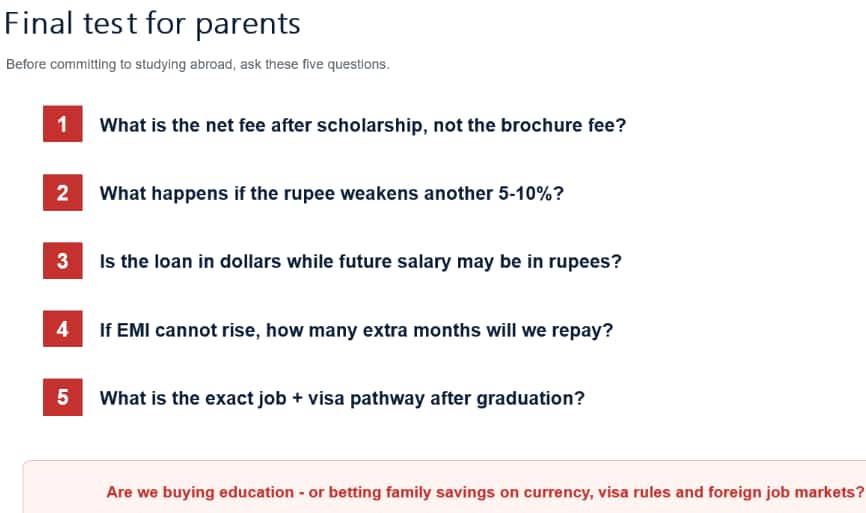

Parents and students are advised to ask key questions about net fees, forex loans, post-study job opportunities and visa/work permit conditions.

The current reality is that living expenses and tuition fees are fixed, but there is uncertainty in the post-study job opportunities and loan repayment. It is important to understand realistic expectations before investing financially in studying abroad.

If you are strong financially and getting admission opportunities in a reputed university, then only consider studying overseas.

Parents and students must calculate the overall expense besides tuition fees.

Particularly ask for the net fees after scholarships instead of a brochure fee.

Analysis of job opportunities & work visa rules and regulations.

Consider the effects of potential rupee depreciation and implications of forex loans.

Studying abroad is a heavenly financial investment where cost is certain, but outcomes are not.

Foreign campuses in India are relatively legitimate and a lower-risk option with scholarship opportunities.

Among top 100 Universities Globally in the Times Higher Education (THE) Interdisciplinary Science Rankings 2026

Among top 100 Universities Globally in the Times Higher Education (THE) Interdisciplinary Science Rankings 2026

Last Date to Apply: 31st July | Ranked #43 among Engineering colleges in India by NIRF | Get Upto 100% Scholarships | Spot Admissions via CUET

100+ Recruiters | 1200+ Placements of 2026 Batch | NBA & NAAC Accredited | Highest CTC 37 LPA

NAAC A+ Accredited | Highest CTC 45 LPA | Scholarships Available

NAAC A+ Accredited | Highest CTC 45 LPA | Scholarships Available